It might just be the right time to sell your condo!

IS IT THE BEST TIME TO SELL YOUR CONDO?!

With the new changes in legislation regarding borrowing just announced, we are seeing a push in entry-level buyer demand. This comes on top of an already pressurized Seller’s market seeing low inventory and fast sales in the strata game. This is mostly due to the local rental crises, where rents have climbed to meet mortgage payments while interest rates are so low. Renters find little quality supply, huge rent increases, and competition for space not unlike the sales market so people are still keen to get in. It seems there will likely be a rush of buyers trying to secure a home before those new rules take effect, limiting their affordability. The rules directly impact First Time Home Buyers so we see the cheaper, entry-level 1, 2 & 3 bedrooms seeing the biggest push in buyer demand. Check out the new rules below and if you are thinking of selling your condo anytime soon – GIVE US A CALL TO CHAT ABOUT IT! It might be a good idea to do it sooner rather than later.

The strata market has remained busy amidst all the negative media buzz surrounding our housing market, while the detached market tells us a different story. Inventory is up and sales are down. The stats show us that this is an excellent time to space upgrade from strata to land, while the sections of the market are more polarized than usual. So is it the best time to sell your condo? If you want some help considering the options, call your friendly neighborhood Realtor, and our team leader, Ruth Chuang at 604-782-2083

NEW MORTGAGE FINANCE RULES

RULE CHANGES – 3 mortgage types to consider

|

A – Loans with less than 20% down (High Ratio)

– These loans require mortgage insurance under the bank act to protect the lender from default.

– The person taking the mortgage pays for the mortgage insurance and it is usually added the the mortgage amount

New Rules:

– All loans will be qualified at the benchmark rate (currently 4.64%) with 25 year amortization

When:

– Starting October 17th, but expect lenders to stop taking applications prior to this date as they have done with past changes

Meaning:

– We used to be able to qualify people using the current five year discounted rate if they took a five year fixed term (now about 2.49%). As we are no longer able to do this, people will qualify for about 20% less mortgage and require roughly 25% more income for the same mortgage as prior to the changes.

B – Loans with 20% or more down that are insured on the back end with CMCH or another insurer:

– Although the buyer is often not aware and rarely pays for the insurance, lenders often insure mortgages with 20% or more down in order to reduce their risk, maintain a lower capital reserve for the same mortgage portfolio and most importantly securitize and sell the mortgages. Securitizing is essentially bundling and selling the mortgages to an investor behind the scenes. The client continues to deal with the lender day to day, but the actual debt has been sold. If the mortgages are insured, the investor or buyer of the mortgage securities is willing to take a lower yield and this then allows the lender to pass on lower rates to the borrower. This tends to provide lower rates and more stability in the marketplace. Here is a good explanation https://www.cmhc-schl.gc.ca/

New Rules:

– Qualifying rate of 4.64% ( it was discounted 5 year rate previously)

– maximum amortization of 25 years (it was 30 years)

– maximum property value of $1M

– Must be owner occupied (rental properties were included previously)

Meaning:

– Many existing programs may be cut or have to find alternative ways of funding – this will take time.

– Reduction in competitiveness in the marketplace

– Possible rate increases due to less competitive marketplace

– Most likely a Larger market share for the big five banks and credit unions

When:

November 30th, 2016

C – Loans with 20% or more down that are not insured on the back end:

– These are loans that a lender keeps on their books and handles the finances in house

New Rules:

– there looks to be no changes to these mortgages at this time

Meaning:

– Lenders use securitization at different levels and the ones that hare more in house funds will be at an advantage.

– The reduction in securitized loans in this segment may see higher rates in the short term – long term is unclear.

We feel the new changes increase the need for client to seek out independent advice from professionals who have access to multiple channels of business. As a broker we have access to large banks, credit unions, monoline lenders, trust companies and private financing entities.

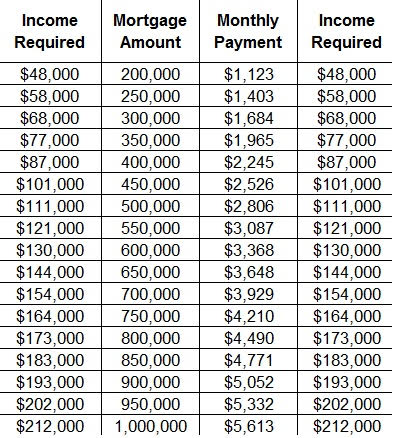

Below is a qualification guide based on the new qualification rate of 4.64% over a 25 year amortization.

|

|

Featured Listings

1923 Parker Street,

Vancouver

Exceptional investment opportunity in the heart of East Vancouver’s sought after Commercial Drive neighborhood. This 3 level walk-up apartment... Read More >

210 4458 Albert Street,

Burnaby

Rare offering at Monticello in the Heights! Perfectly situated on the front side of the building, this bright upper-level townhome blends space,... Read More >